The violent drawdown sweeping across tech—cleaving over 4% from the Nasdaq today—is not a crisis of technological innovation. It is a mathematical reckoning. Investors are stripping the premium from long-duration equities as the market accepts that sticky inflation will keep the discount rate elevated. When capital costs refuse to bend, multiples on future growth must break.

For the past several quarters, mega-cap tech served as a pseudo-defensive haven. The assumption was that dominant balance sheets could outrun higher yields. But as the Federal Reserve under Kevin Warsh is forced to confront a higher-for-longer rate path, that immunity is fading. The market is suddenly evaluating software and semiconductor conglomerates purely on their sensitivity to the risk-free rate.

The Fed's Terminal Yield Ceiling

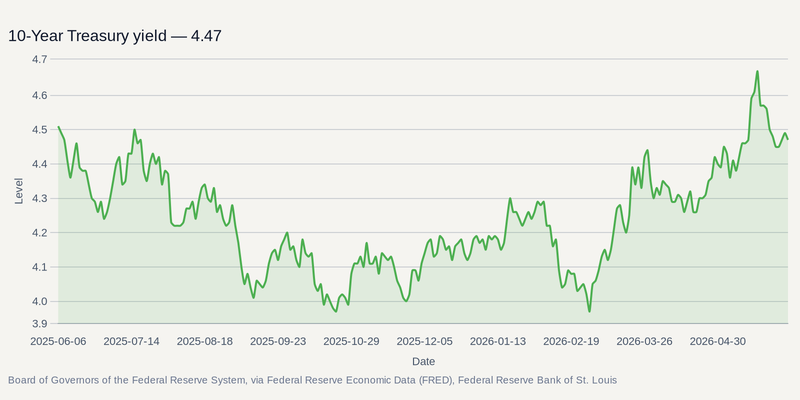

The link between central bank policy and software valuations is direct. Growth stocks live on cash flows projected years into the future. When the 10-year Treasury yield climbs and stays elevated, those distant cash flows lose their value in today's dollars.

This dynamic forces a rotation out of Information Technology names that priced in aggressive rate cuts . With the 10-year yield hovering near 4.5%—well up from its sub-4% lows in February—the math has changed. Capital is draining out of high-multiple SaaS vendors and speculative hardware, redirecting toward businesses that generate immediate free cash flow.

Growth’s Vulnerability to an Economic Surprise

The consensus assumes rates stay high because the economy is strong enough to take the hit. The real threat to this bearish tech view is a sudden macroeconomic crack. If consumer spending stalls or the labor market fractures, a flight to safety will drag yields down fast.

In that scenario, long-duration assets snap back. The high-beta tech names leading today's selloff in QQQ would re-rate higher as discount rates fall. But betting on a sudden economic collapse to rescue software multiples means fighting the Fed's current policy path.

Where Capital Hides When Discount Rates Bite

Until the yield curve signals a deflationary panic, survival means shortening duration. Markets are screening for current cash yield, not total addressable market promises.

This shift supports defensive value and established Financials, where higher rates boost net interest margins instead of wrecking valuations. Within tech, focus narrows to mega-caps returning capital today—like AAPL and MSFT—while the rest of the sector resets to historical valuation norms.