Wall Street broadly bounced on Monday, but the true structural shift arrived disguised as a routine distribution deal. Comcast formally bridged its streaming service, Peacock, directly into YouTube Primetime Channels. Paired with Comcast's newly announced plan to spin off NBCUniversal and Sky entirely—following the completed separation of its traditional cable networks earlier this year—the move marks a definitive industry capitulation. Legacy media is abandoning the decades-old dream of total vertical integration—owning both the content and the proprietary technology pipes—to prioritize raw content monetization on big tech's massive distribution architecture.

Dismantling the Walled Gardens

For years, traditional studios bled cash attempting to build standalone tech platforms capable of rivaling Netflix. Today, the Streaming Media & Content Delivery sector is actively unwinding that strategy. By plugging directly into YouTube via Primetime Channels, Peacock captures reach without the friction and crippling customer acquisition costs of relying solely on its standalone app. Media executives are finally conceding that software engineering and cloud distribution are not their core competencies. Instead, global streaming is aggressively shifting toward hybrid monetization models, relying on established tech aggregators to deliver eyeballs while studios focus on what they do best: producing the entertainment itself.

The $111 Billion Premium Floor

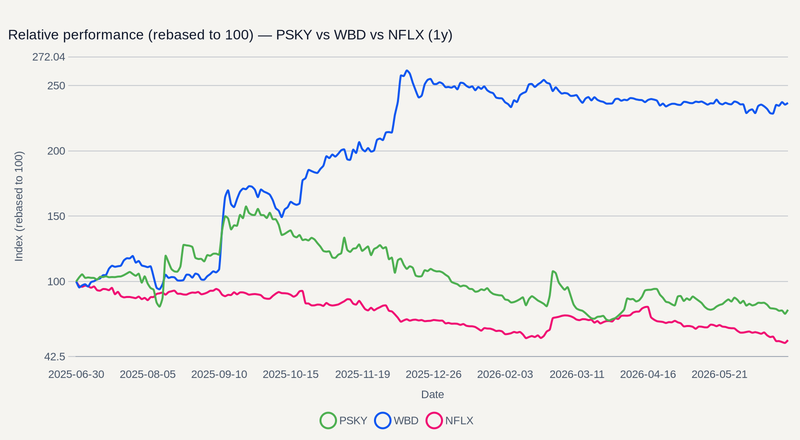

As the distribution pipes become commoditized, the underlying intellectual property commands an immense premium. Look no further than Paramount Skydance and its definitive $110.9 billion agreement to acquire Warner Bros. Discovery. While the saga began with a hostile $108.4 billion bid in December 2025 , the final agreed-upon price of $31 per share establishes a massive valuation floor for premium content libraries. Rather than fighting big tech on software engineering, Paramount is assembling an intellectual property juggernaut capable of dominating direct-to-consumer and linear advertising.

This consolidation forces rivals to adapt. Disney finds itself reassessing its M&A defenses, while Netflix pivots its cash reserves toward alternative growth vectors after bowing out of the Warner Bros. bidding war entirely in February 2026—pocketing a cool $2.8 billion breakup fee in the process . Though state-level regulatory reviews remain, the Department of Justice cleared the transaction in June 2026, paving the way for a new era of media consolidation.

Integration Hurdles and Regulatory Gauntlets

Merging these distinct entertainment empires carries extreme structural risks. The proposed combination of Paramount and Warner Bros. Discovery must integrate live sports and free ad-supported streaming properties with legacy linear networks and premium studios . Historical realized price volatility during media mega-mergers suggests initial hype frequently outpaces operational reality. M&A catalyst events traditionally exhibit a bullish tilt on announcement, but flatline trading often follows as the massive debt loads required to finance the deals drag on balance sheets.

Moreover, while the U.S. Department of Justice cleared the transaction in June 2026, antitrust scrutiny remains a hurdle for deal completion. Regulators are actively evaluating whether this level of consolidation will restrict consumer viewing choices and hike subscription costs . The UK’s Competition and Markets Authority and the European Commission are conducting deep reviews, while a coalition of state attorneys general—led by California—continues to investigate a potential legal challenge.

Tracing the Catalyst Clocks

The sector now pivots from deal euphoria to regulatory reality. Scouter’s catalyst data highlights two critical windows this summer. First, Netflix reports Q2 earnings in July, detailing its strategic capital reallocation. Then, in August, the market faces dual flashpoints: Paramount’s Q2 guidance on synergy targets and the UK’s Competition and Markets Authority (CMA) antitrust decision deadline. Investors evaluating these setups should weigh the allure of massive integrated advertising packages against the reality of saturated subscriber growth. The game is no longer about who builds the best streaming app, but who controls the most indispensable stories.