Michael Burry has trained his sights on the AI infrastructure trade, packaging new short bets against heavy machinery and a major chip ETF (because nothing says 'secular growth' like shorting Caterpillar at a multi-decade high price-to-sales multiple) while economists sound alarms over a potential bust. But treating this as a simple "AI is over" narrative misses the actual transmission mechanism playing out in markets. The structural bottleneck has migrated from physical foundries to the software application layer. Over the last two years, Software-as-a-Service vendors engaged in a massive hardware arms race, purchasing compute to build models without a clear path to sustainable unit economics. Now, the bill is coming due—presenting a critical risk-management scenario for software investors.

The $2 Trillion ROI Disconnect

The math for enterprise software is undergoing a brutal recalibration. At the beginning of last year, the median revenue multiple for software firms sat comfortably above 7x; today, it has compressed below 5x . Investors are no longer willing to fund endless computing expenditures without seeing reciprocal top-line expansion.

Look at ORCL for the exact blueprint of this reckoning. The database giant recently posted a record $638 billion backlog and projected a massive 58% to 64% growth in cloud revenue for the upcoming quarter. The market's response? Shares dumped more than 10% in a single session as investors fixated on the sheer scale of capital expenditures (management is forecasting a net capex outlay of about $70 billion for fiscal 2027—proving that building the AI future is a very, very expensive hobby) and the financing costs required to sustain that growth .

When the companies buying the chips are punished for buying the chips, the entire hardware valuation stack comes under pressure. The Information Technology sector is currently flashing a dominant 54.1 percent bear rate in Scouter's data as tech firms struggle to clear sky-high quarterly expectations, frequently triggering aggressive sell-the-news reactions.

Bridging the Application Gap

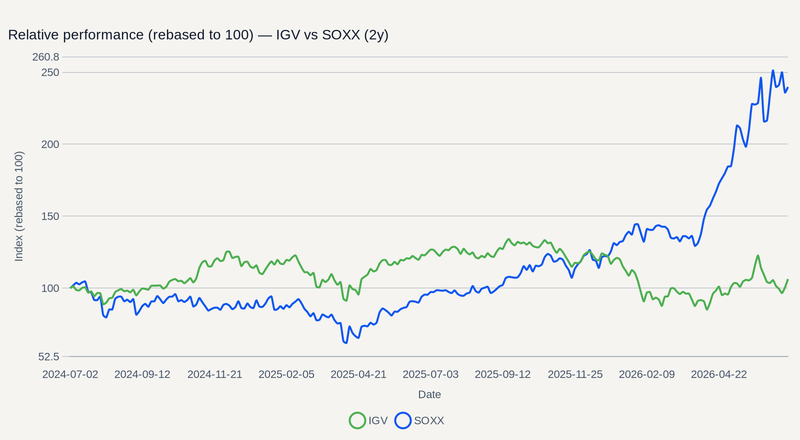

Despite the broad multiple compression, capital isn't entirely abandoning the software space—it is rotating. Funds are systematically shifting positions away from overextended hardware names (because how many GPUs can one planet actually buy?) and back toward vertical AI applications that exhibit healthier valuation structures .

This rotation targets companies actively proving they can extract cash from end-users. Retail and ecommerce buyers are rapidly accelerating their SaaS investments to optimize omnichannel strategies and data-driven marketing, treating AI not as an experimental toy but as a core operational utility . This pivot toward hybrid cloud models and domain-specific applications has kept a focused 53.8 percent bull rate alive in Scouter's quantitative models for names with clear monetization roadmaps. SNOW has already shown early success in this transition, driving tangible top-line contributions from its integration of AI analytics (specifically its Cortex Code and Snowflake Intelligence tools, which helped management raise full-year guidance).

The Summer Earnings Gauntlet

The next eight weeks will explicitly test whether software vendors can bridge this capex-to-revenue divide. The timeline is unforgiving.

NOW faces the market first on July 22, serving as a critical bellwether for enterprise digital transformation budgets. A week later, hyperscaler MSFT is expected to report on July 29, offering the definitive read on whether broad enterprise seat upgrades are actually generating free cash flow. Finally, CRM is expected to report on August 26, testing whether proprietary data advantages can successfully defend CRM market share against cheaper vertical upstarts.

The counter-narrative to this SaaS margin crunch is straightforward: if these heavyweights prove they can command premium pricing for AI-augmented software seats, margins will rapidly expand. In that scenario, today's punishing capex transforms from a balance-sheet anchor into an insurmountable competitive moat. Until those earnings prints land, the burden of proof rests entirely on the software vendors to justify the hardware boom.